The FINRA New Member Application – A Comprehensive Guide

A FINRA New Member Application, or NMA, is subject to a process that can be onerous and confusing, but the good news is that it has been streamlined over the last few years. And believe it or not, delays often have more to do with the content and quality of the application than with FINRA itself.

A FINRA New Member Application, or NMA, is subject to a process that can be onerous and confusing, but the good news is that it has been streamlined over the last few years. And believe it or not, delays often have more to do with the content and quality of the application than with FINRA itself.

One of the most frequent reasons for a delay in the FINRA new member application process is that the applicant has submitted an incomplete or inaccurate application. Substantial delays can occur as a result of a failure to complete the required licensing examinations, submission of incomplete documentation, or an inadequate business plan. Getting the application filed in good order is a critical part of the process.

FINRA will reject an application if it is not complete because its rules provide that applications, when filed, should be “substantially complete.” This requirement places the burden almost entirely on the applicant to produce what FINRA wants to see. So how long does it take?

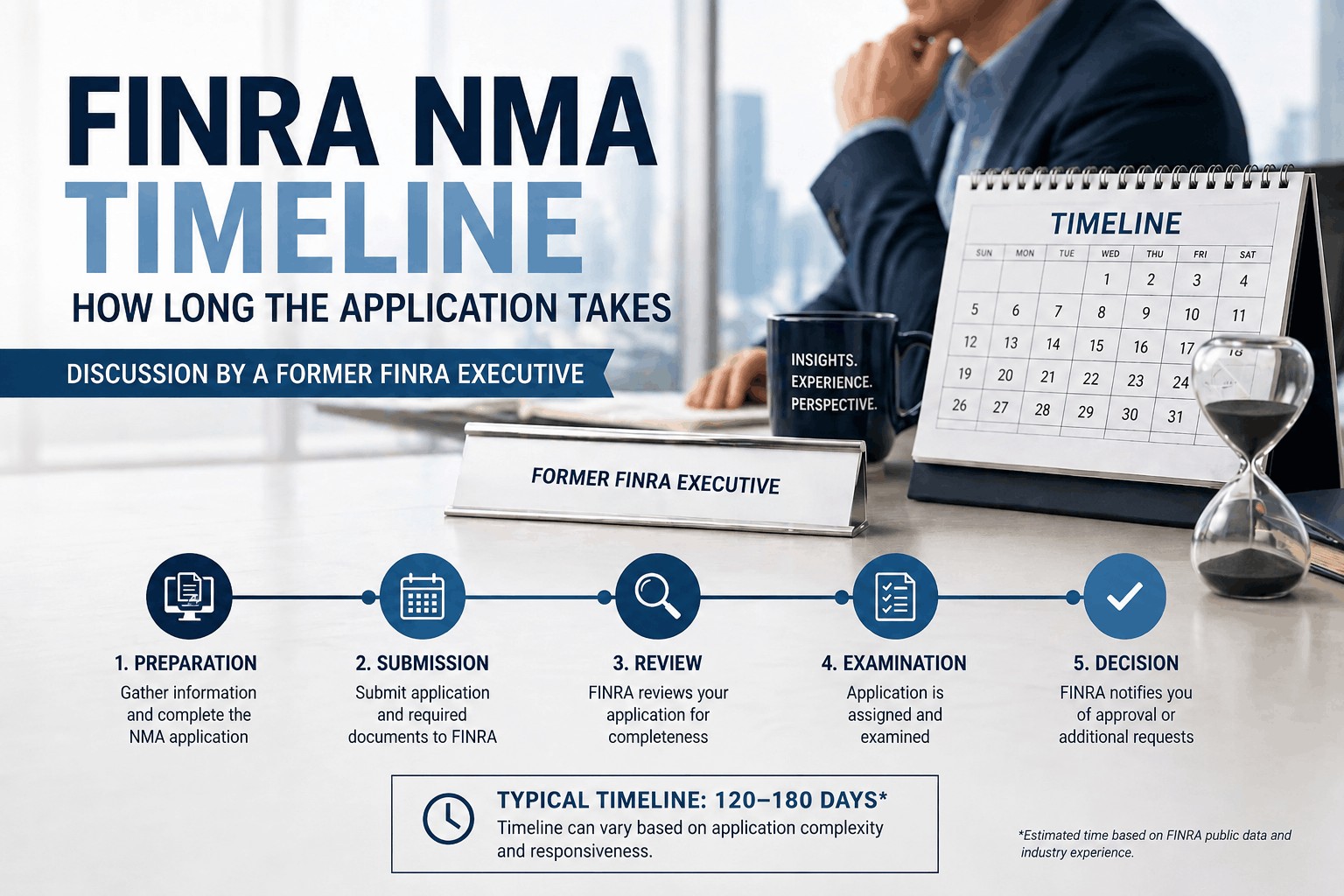

Quick answer: FINRA is required by rule to decide on a substantially complete New Member Application (NMA) within 180 calendar days of its acceptance. In practice, straightforward applications are typically resolved in a shorter time period. Most applications land somewhere between four and nine months from filing to approval. Complex business models, incomplete filings, or slow applicant responses can push the timeline past that range.

If you are a founder, compliance officer, or counsel preparing to launch a broker-dealer, the question you really want answered is not only “what does the rulebook say” but “how long will my application take, and what can I do to shorten it?” This guide answers both. It is written from the perspective of a former FINRA Regional Director who has overseen hundreds of NMA reviews and, on the consulting side, has shepherded applicants through the process from the first pre-filing meeting to the executed membership agreement.

The 180-Day “Rule”: What FINRA Is Actually Obligated to Do

Under FINRA Rule 1014, FINRA’s Membership Application Program (MAP) Group must issue a written decision on an NMA within 180 calendar days after an application is deemed substantially complete. The clock does not start the moment you click “submit” on Form NMA in FINRA Gateway. It starts when MAP determines your application package contains enough information to support a meaningful review.

Two important nuances flow from this:

The “substantially complete” gate can add weeks to your calendar before day one. When an application is submitted, MAP conducts an initial screen. If the package is not substantially complete, the applicant is given five business days to cure the deficiency or the application is rejected, and the fee is refunded, less $500. If the package passes the screen, MAP generally has 30 days to complete a preliminary review and issue the first written request for additional information. That first request typically arrives three to four weeks after filing.

The 180-day clock can be extended. If MAP shows good cause, the FINRA Board may extend the 180-day limit by up to 90 additional days. More commonly, the applicant and MAP agree in writing to a later decision date, typically because the applicant needs more time to respond or because the business model raises novel regulatory questions that warrant deeper review.

So while “180 days” is the headline number most consultants cite, the honest answer to how long your NMA will take is: 180 days is the maximum FINRA gives itself once your application is in order, not the amount of time you should plan for.

The Realistic NMA Timeline, Phase by Phase

Here is how the calendar typically breaks down for a well-prepared applicant:

Phase 1: Pre-filing preparation, 60–120 days before filing

Before Form NMA is ever submitted, the applicant must reserve a firm name, obtain a CRD number, designate a Super Account Administrator, file Form BD with the SEC, file Forms U4 for proposed registered persons, file Form BR for each proposed branch location, and, critically, have principals sit for and pass their qualification exams, typically the SIE plus series-specific exams such as the Series 24, Series 27, Series 7, Series 79, or others, depending on the business model. Written Supervisory Procedures, a detailed business plan, financial projections, and a Business Continuity Plan must all be drafted and internally consistent.

This phase is almost always the single biggest predictor of how long your NMA will take. Applicants who treat pre-filing as a checklist exercise file thin applications and pay for it with multiple rounds of information requests. Applicants who treat pre-filing as the substantive work of the NMA often end up with decisions in 100–130 days.

Phase 2: Substantially complete review, Days 1–30

After Form NMA is filed through FINRA Gateway, MAP screens the package. If anything required by FINRA Rule 1013(a) is missing, for example a complete BCP, a detailed business plan, ownership charts with exact percentages, financial statements within 30 days of filing, clearing agreements, or written supervisory procedures, the application may be deemed not substantially complete. These situations must be cured promptly.

Phase 3: First information request and applicant response, Days 30–90

Once the application is accepted, an examiner is assigned. The examiner prepares a detailed written request for additional information, which is typically issued within 30 days of acceptance. The applicant then has 60 calendar days to respond. Experienced consultants almost always recommend responding in 15–30 days instead of taking the full 60. Every day you hold the pen is a day the clock keeps running.

Phase 4: Second and sometimes third information request, Days 90–150

After reviewing the applicant’s response, MAP may issue a second written request. Applicants typically have 30 days to respond. For more complex applications, especially those involving novel business models, complicated ownership, or disclosure history, a third request letter, or “round” of questions as it is commonly referred to, is not unusual.

Phase 5: Membership interview, Days 120–160

Before any decision is issued, FINRA must conduct a membership interview with the applicant’s principals. FINRA must give at least seven days’ notice of the interview. The interview is where MAP walks through the application against the 14 standards of admission, surfaces any remaining concerns, and shares any information MAP has obtained from outside sources that it intends to rely on. By the time the interview happens, most of the heavy lifting should be done. This is not the place to be learning about your own business plan.

Phase 6: Decision and membership agreement, Days 150–180

Under Rule 1014, a written decision must be served within 30 days after the later of (a) the membership interview or (b) the filing of additional information. The decision can grant the application, grant it with restrictions, or deny it. The approved business lines and any restrictions are documented in a Membership Agreement that must be executed and returned through FINRA Gateway. Approval does not become effective until the executed agreement is received.

Expedited review

For a narrow set of applications, MAP may agree to expedited review, roughly a 100-day cycle for NMAs rather than 180. Expedited treatment is discretionary and generally reserved for straightforward applications with experienced principals, no disclosure history, limited business scope, and sophisticated or institutional client bases. If your model checks those boxes, raising expedited review, sometimes called “fast-track” review, in a pre-filing meeting is worth the conversation.

The Six Factors That Most Influence Your NMA Duration

Over two decades of working with NMAs, a handful of variables explain the vast majority of timeline variance:

- Completeness and internal consistency of the initial filing. This is by far the largest lever. An application in which the business plan says one thing, the WSPs say another, and the financial projections assume a third version of the business is going to generate round after round of information requests. FINRA’s rules place the burden on the applicant to produce a substantially complete package, and while MAP rarely rejects applications outright, it will ask questions until the record is coherent.

- Complexity of the business model. A single-principal M&A advisory shop serving institutional clients is not the same application as a carrying firm clearing crypto ATS transactions for retail investors. Digital assets, alternative trading systems, omnibus arrangements, proprietary trading, market making, and retail customer funds each add substantive review time because they implicate additional rules, exam frequencies, and capital considerations.

- Experience and background of the proposed principals. FINRA Rule 1014(a)(10)(D) requires that each person who will discharge a supervisory function have at least one year of direct experience or two years of related experience in the area to be supervised. Where a proposed principal’s experience is thin, indirect, or stale, expect delays, and in some cases denial. Disclosure history on any principal, including regulatory actions, arbitrations, unpaid awards, or terminations for cause, triggers presumptions against approval that the applicant must rebut on the record. I often work with clients who do not yet have principal licenses. That is not a deal breaker, but we must show their experience is significant.

- Ownership structure. Complex ownership, including foreign owners, multiple holding companies, trusts, owners with control person histories at other broker-dealers, or lenders holding 5% or more of net capital, requires additional documentation. MAP typically requests governing documents for any entity holding 10% or more. I often work with applicants owned by entities or even private equity. These can get more complex, but there are solutions.

- Applicant responsiveness. FINRA’s clock includes time FINRA is holding the file, but applicant response time is real calendar time. Applicants who take the full 60 days for the first response and the full 30 days for every subsequent request effectively add three or four months to their own timeline before FINRA does anything. We work to reduce the turnaround time and the number of “rounds” of questions.

- Quality of written supervisory procedures and the business plan. Generic, off-the-shelf WSPs that do not match the specific business model are a consistent source of follow-up. Business plans that cannot reconcile projected revenues with headcount, technology spend, and net capital requirements invite scrutiny of the firm’s operational readiness under Standards 4, 5, 6, and 10 of Rule 1014.

What Does a FINRA NMA Cost?

The cost of starting a FINRA broker-dealer varies considerably with the size and complexity of the proposed business, but the major categories are reasonably consistent. The fees described below should be treated as the foundation of a budget rather than the full picture, since each firm’s specific business model will introduce additional line items.

FINRA Application Fee

FINRA’s NMA filing fee is tiered based on the proposed size of the broker-dealer, measured by the number of registered persons at the start of operations. The fee ranges from $7,500 for firms with up to 10 registered persons up to $55,000 for firms with more than 5,000 registered persons. The vast majority of NMAs involve firms in the smallest tier, so $7,500 is the most common application fee.

Smaller Fees That Add Up

Beyond the application fee itself, an applicant pays a series of smaller fees that collectively represent a meaningful budget line:

- Branch office registration: currently $105 initial registration fee plus $75 system processing fee per branch, subject to FINRA’s one-branch waiver

- Disclosure processing fee for items reported on Form U4: $155 each

- Fingerprint processing: currently $30 for electronic submissions and $40 for hardcopy submissions, plus any separate vendor collection fee

- Principal and representative application fees: $125 per person

- Series 7 examination fee: $395 (other exam fees vary)

- State registration fees for registered representatives: vary by state ($190 in New Jersey, for example)

- State registration fees for the broker-dealer itself: vary by state ($550 in Pennsylvania, for example)

- MSRB fee if the firm will engage in municipal securities business: registration fee of $1,000 plus annual fee of $1,000

Capital Requirements

FINRA requires that a broker-dealer maintain minimum net capital, with the specific minimum depending on the firm’s business model. The lowest minimum is $5,000, applicable to certain limited business types; many firms have higher minimums. FINRA generally expects firms to maintain capital at 120% of their minimum requirement as an operational buffer — so a firm with a $5,000 minimum should be capitalized at $6,000 or more to avoid early supervisory attention. FINRA also requires applicants to demonstrate financial wherewithal sufficient to cover twelve months of initial fixed operating expenses, which for most firms is the more substantial capital constraint.

Insurance, Bonding, and Audit

FINRA requires that broker-dealers maintain a fidelity bond. Errors and omissions insurance is not required by FINRA but is strongly advisable and is effectively required by most clearing firms and many state regulators. Broker-dealers must also contract for an annual certified audit by a PCAOB-registered CPA firm. Audit costs have increased substantially in recent years and now typically range from several thousand dollars to tens of thousands depending on the firm’s complexity.

Ongoing SIPC Fees

SIPC charges 0.0015 of Net Operating Revenues on an ongoing basis. This is a small percentage but should be factored into the firm’s financial planning from the start.

Clearing Firm Deposit

Firms that will clear customer transactions through another broker-dealer – rather than dealing only with mutual fund, annuity, and similar product providers directly, or selling only private placements — will need a clearing agreement. Clearing firms require a deposit that typically ranges from $10,000 to several million dollars, depending on the proposed business.

Consulting and Legal Fees

Most applicants engage outside help. Regulatory consultants typically charge a flat fee for handling the NMA from initial preparation through FINRA approval. Fees vary widely depending on the consultant’s experience, the complexity of the proposed business, and the scope of work included. A serious consultant’s quote should include everything required to satisfy FINRA’s application process: written supervisory procedures, business continuity plan, AML compliance program, Regulation S-P compliance program, Regulation S-ID compliance program, and the various other required policies. Legal fees for incorporation and ancillary corporate matters are separately paid to your attorney.

Total Budget

For a small broker-dealer — fewer than 10 registered persons, modest business scope — a reasonable rule of thumb is a minimum initial capital investment between $125,000 and $175,000, in addition to professional fees. Firms with more complex operations, extensive technology requirements, multiple branch offices, or higher capital requirements should expect to invest substantially more. Registering a broker-dealer is not an inexpensive proposition; the rewards can be substantial, but the entry costs are real and should be planned for from the start.

Who Must Register as a Principal?

One question that comes up in nearly every NMA involves the registration status of owners, officers, and directors. FINRA’s requirements here are specific, and they often surprise first-time applicants — particularly those who are coming from outside the securities industry or who assume that ownership without operational involvement avoids registration.

The General Rule

FINRA requires registration as a principal for anyone “actively engaged in the management of the member’s investment banking or securities business, including supervision, solicitation, conduct of business, or the training of persons associated with a member for any of these functions.” This expressly includes sole proprietors, officers, partners, managers of offices of supervisory jurisdiction (OSJs), and in many cases corporate directors.

The activities that consistently push someone across the line into the principal registration requirement include hiring and firing, setting or implementing policy, negotiating or executing agreements on the firm’s behalf, directing other employees’ actions, participating in management or executive committee meetings, and holding oneself out as a person with authority to make decisions for the firm.

The Narrow Exception for Outside Directors

FINRA recognizes that a director who is truly outside the broker-dealer’s securities business and not actively engaged in management may not require principal registration based on title alone. A truly outside director who attends quarterly board meetings, reviews reports prepared by management, and provides general oversight without operational involvement can typically avoid principal registration.

The exception is narrower than many applicants assume. Outside-director status is difficult to reconcile with being registered with the broker-dealer in another capacity. A director who holds a representative registration with the firm because the person intends to participate in client or securities business generally should expect FINRA to require principal registration. In practical terms, the representative registration undercuts the argument that the director is merely an outside director providing passive board-level oversight.

FINRA understands that not all registrations will be in place upon filing of the NMA. An applicant may sponsor proposed principals to sit for their qualification examinations using the pending NMA as the sponsor, with reasonable time from the filing date to pass. There are work-arounds in specific situations if the exam window cannot accommodate a particular individual’s schedule.

Practical Advice

My standard advice to owners, shareholders, and others who will have any role in decision-making is to get the license. The cost of unnecessary registration is modest; the cost of running into FINRA’s principal registration requirements mid-application is substantial. Applicants who plan to keep owners out of principal registration based on optimistic readings of the “outside” exception often end up having to register those individuals anyway, with attendant delays in the NMA process.

What Is FINRA Actually Evaluating? The 14 Standards of Admission

Form NMA is organized around the 14 standards in FINRA Rule 1014(a), and every day of MAP’s review is spent mapping what you have submitted to what those standards require. Understanding how the standards drive the review will help you file an application that closes quickly.

Stated in practical terms, the 14 standards require the applicant to demonstrate:

- The application and supporting documents are complete and accurate.

- The applicant and its associated persons have all required state, federal, and SRO licenses and registrations.

- The applicant and its associated persons are capable of complying with the federal securities laws, the rules thereunder, and FINRA rules.

- Contractual and business arrangements, including clearing, custody, service providers, and intercompany arrangements, are adequate and disclosed.

- The applicant has adequate facilities to conduct the proposed business.

- Communications and operational systems, including a compliant Business Continuity Plan under FINRA Rule 4370, are in place.

- The applicant has adequate financial resources and net capital.

- The applicant’s recordkeeping system satisfies SEA Rule 17a-3 and 17a-4 and related requirements.

- The applicant has developed written supervisory procedures reasonably designed to achieve compliance.

- The applicant has adequate supervisory structure and personnel, including at least two registered principals, plus a Financial and Operations Principal, with the required direct or related experience.

- The applicant’s books, records, and home office are subject to FINRA inspection.

- The applicant has a recordkeeping system capable of producing records in the formats required by rule.

- The applicant has taken steps to establish compliance with anti-money-laundering obligations, customer identification requirements, and other regulatory programs.

- The application is otherwise consistent with the federal securities laws, the rules thereunder, and FINRA rules.

If the applicant, its control persons, principals, or 5% lenders are the subject of certain regulatory actions, criminal proceedings, unpaid arbitration awards, or terminations for cause, a presumption of denial attaches under Rule 1014. The application can still be approved, but the applicant bears the burden of overcoming that presumption on the record, which takes time, documentation, and typically careful legal and regulatory positioning.

The Rebuttable Presumption of Denial

Before investing the time and resources required to file a New Member Application, prospective applicants should understand a specific provision of FINRA’s membership rules: Rule 1014(b)(1) establishes a presumption that an application should be denied when certain enumerated events are present. This is one of the most consequential provisions in the NMA process, and one of the least well understood by applicants encountering FINRA membership for the first time.

The circumstances that trigger the presumption are set out in Rule 1014(a)(3)(A) and (C) through (E). At a high level, they include:

- A permanent or temporary adverse action by a state or federal authority or self-regulatory organization with respect to a registration or licensing determination involving the applicant or an associated person.

- Pending, adjudicated, or settled regulatory actions or investigations involving the SEC, CFTC, a federal, state, or foreign regulatory agency, or a self-regulatory organization.

- Adjudicated or settled investment-related private civil actions for damages or injunctions.

- Criminal actions, other than minor traffic violations, that are pending, adjudicated, or that resulted in a guilty or no contest plea.

- Unpaid arbitration awards, other adjudicated customer awards, or unpaid arbitration settlements involving the applicant, its control persons, principals, registered representatives, other associated persons, certain lenders, or certain other members with which those persons were associated in a control or lending capacity.

- A termination for cause, or a permitted resignation after investigation, involving an alleged violation of securities laws, SRO rules, or industry standards of conduct.

- Remedial action imposed on an associated person by a state or federal authority or self-regulatory organization, such as special training, continuing education requirements, or heightened supervision.

The existence of one of these circumstances does not mean the application must be denied. Rule 1014(b)(1) expressly provides that the presumption is rebuttable. The applicant may overcome the presumption by demonstrating that it can satisfy each of the standards for admission in Rule 1014(a), notwithstanding the triggering event.

That said, applicants with any of these factors in their background should not assume the issue will be overlooked. The right approach is to address triggering circumstances proactively in the application itself, on the record, before MAP staff have to ask. This accomplishes two things: it demonstrates that the applicant has thought carefully about the issue, and it puts the applicant’s framing of the circumstances in front of MAP from the outset rather than in a defensive response to a later question.

What Rebutting the Presumption Looks Like

Overcoming the presumption is a substantial undertaking. The work involved depends on the nature of the triggering circumstance:

Older or isolated events with clear context. Sometimes the presumption can be overcome through a thorough written explanation of the circumstances, the steps taken to address what happened, and the evidence that the issue is not indicative of ongoing risk. This is most likely to succeed when the event is older, involved a single isolated matter rather than a pattern, and was followed by a meaningful period of clean regulatory history.

More recent or serious events. When the triggering circumstance is more recent, more serious, or part of a pattern, more substantial work is generally required. This may include restructuring aspects of the proposed firm — changing the ownership structure, modifying the supervisory plan, removing or repositioning specific personnel, or narrowing the proposed scope of business. The goal is to address the underlying concern that gave rise to the presumption, not just to argue around it.

Documentation from third parties. Rebuttals often benefit from supporting documentation — court records, regulatory orders that have been satisfied, evidence of remediation, arbitration or settlement documentation, proof of payment, updated disclosure records, or in some cases letters from prior employers or supervisors. The strength of the written record matters considerably.

The first step in any case is understanding exactly what triggered the presumption and what concern that triggering circumstance reflects from FINRA’s perspective. Rebuttals that address the surface facts without addressing the underlying concern tend not to succeed. Rebuttals that meet the concern directly, with documentation and, where appropriate, structural changes can succeed even on difficult records.

Applicants with any of these factors should plan for a longer NMA timeline and should expect that the depth of MAP’s review will be greater than for an applicant with a clean record. This is not a reason to avoid filing — it is a reason to file thoughtfully, with the presumption addressed head-on rather than left for FINRA to raise.

What Makes MAP Move Faster — Practical Insights

A few patterns show up consistently in the NMAs that resolve near the 100-day mark:

- Pre-filing meeting with MAP. Applicants with novel business models, complex ownership, or any disclosure history should almost always request a pre-filing meeting with MAP. It surfaces issues before they become written deficiencies. FirstMark routinely schedules these calls in connection with any application.

- One coherent narrative. The business plan, WSPs, financial projections, organizational chart, and clearing/service agreements all tell the same story about what the firm will do, who will do it, and how much it will cost.

- Principals in place and licensed at filing. Exam failures and last-minute principal substitutions are among the most common reasons NMAs stall.

- Bank statements and financial documents that match the projections. FINRA does not accept redacted bank or brokerage statements and will check that source-of-capital documentation actually supports the funding described in the business plan.

- Fast, complete responses to information requests. Responding in 15–20 days with a full answer, rather than in 60 days with a partial answer, is the single most controllable lever on your timeline. The goal is to reduce the turnaround time and the number of “rounds” of questions.

- A realistic scope. Firms that apply for every activity they might someday want to conduct face broader review than firms that apply for the scope they will actually launch with. Adding lines of business later through a Continuing Membership Application (CMA) under Rule 1017 is often faster than trying to get everything approved in the NMA.

What Happens After Approval

Approval is usually conditional. Most approved applicants receive a Membership Agreement that reflects specific restrictions tied to the business plan, including number of registered persons, lines of business, capital thresholds, customer account handling, or other tailored limitations. The applicant has 25 days to return the executed agreement through FINRA Gateway; failure to do so can cause the application to lapse.

Once the agreement is signed, state registrations must be completed before business commences in each jurisdiction. State timelines vary widely and can add weeks or months on top of the FINRA process, so coordinating state registrations in parallel with the NMA is essential.

Frequently Asked Questions

How long does a FINRA New Member Application take on average?

Most NMAs take between four and nine months from filing to approval. FINRA’s rule limits its review to 180 days from the date the application is deemed substantially complete, and MAP can process simple applications on an expedited basis in roughly 100 days. FINRA can also request extensions.

Can FINRA take longer than 180 days to decide on an NMA?

Yes. The 180-day limit can be extended by up to 90 days if MAP shows good cause to the FINRA Board, and the applicant and MAP can also agree in writing to a later decision date. It is common for complex applications to exceed 180 days by mutual agreement.

What does “substantially complete” mean for a FINRA NMA?

An application is substantially complete when it contains enough information for MAP staff to conduct a meaningful review. Required items include Form NMA, Form BD, Forms U4, a detailed business plan, financial statements within 30 days of filing, written supervisory procedures, a Business Continuity Plan, and ownership documentation. Missing or inconsistent information is the leading cause of rejection at this stage.

What is the fastest a FINRA NMA can be approved?

Under MAP’s expedited review framework, straightforward applications can be decided in approximately 100 days. In practice, applications approved at the low end of the range tend to involve experienced principals, limited business scope, institutional client bases, clean disclosure histories, and thorough pre-filing preparation.

What causes delays in the FINRA NMA process?

The most common delays are incomplete initial filings, inconsistent documentation, principals who have not yet passed qualification exams, disclosure history on principals or owners, complex ownership structures, novel business models, especially involving digital assets or ATS functionality, slow applicant responses, and material changes to the proposed business during review.

Do I need a consultant to file a FINRA NMA?

A consultant is not required, but an experienced NMA consultant or regulatory counsel can meaningfully shorten the timeline by producing a substantially complete initial package, anticipating MAP’s questions, and maintaining consistency across the business plan, WSPs, and financial projections. The investment typically pays for itself in reduced months of pre-revenue overhead while approval is pending and in getting the new broker-dealer off to the right start by avoiding mistakes that can be costly.

How much does a FINRA NMA cost?

FINRA’s NMA filing fee ranges from approximately $7,500 to $55,000 depending on firm size, with additional costs for state filings, Form BD filings, exam fees, fingerprinting, and required capital. Most small broker-dealers should budget $125,000–$175,000 in initial capital plus professional fees.

What happens if my FINRA NMA is denied?

The decision letter will explain in detail which of the 14 standards the applicant failed to satisfy. The applicant may seek review before the National Adjudicatory Council (NAC) under Rule 1015 and, beyond the NAC, may apply for SEC review under Rule 1019. An applicant can also withdraw and refile a new application that addresses the deficiencies identified.

Talk to an Expert Before You File

Every month your NMA sits in review is a month of rent, salaries, technology, and compliance overhead with no revenue offsetting it. The most expensive NMA is the one that takes twelve months because the initial filing was thin.

Mitchell Atkins, CRCP, is a former FINRA executive and the founder of FirstMark Regulatory Solutions. FirstMark assists broker-dealer applicants with FINRA New Member Applications, Continuing Membership Applications, written supervisory procedures, business plans, supervisory structure, and regulatory strategy. If you are considering a FINRA broker-dealer registration and want a candid assessment of your likely timeline, contact FirstMark or call 561-948-6511 for a confidential consultation.